As the family this summer, I was instructed to get a family-friendly car. My 2005 vintage Smart car wasn’t good enough anymore... So I went for an electric one (EV). I do not drive much as I mostly stay in the city and travel via train or plane for longer distances. I probably do five or so longer yearly car trips, in the 500-1000km range.

Like the internet, electrification is happening fast and creating a huge wave of decentralisation. It is about much more than EVs. Homes are becoming these ‘mini utilities’ that make power from the sun and use it to power themselves. You can store and trade it. And Europe is leading it.

A smartphone on four wheels

Once you have driven an EV, Retention will be high. It is a bit like using a smartphone vs. an analog phone. Plus, there are fewer maintenance costs; you can leave it to charge nearby or at home if possible, there is automatic braking, etc. Yes, the experience of an analog phone was kind of cool, but a smartphone is just so much better--a no-brainer.

Driving an EV is a bit like sitting in a smartphone on four wheels. The car UX has been completely rethought. It is a computer, first and foremost. Amazing things can be done, like over-the-air software upgrades, various new communications features with the car, self-driving capabilities, and so on. We have seen this story play out across many devices, from phones, to TVs, light switches, thermostats, etc. Cars play an important role for most people, probably only second to smartphones. I expect the impact to be substantial. Think about car insurance, transportation in general, cross-device software UX, etc.

Range anxiety and battery lifetime

The biggest argument for not buying an EV, besides the different driving experience, is the ‘range anxiety.’ It is the fear that there are not enough charging stations and that an EV will not have enough battery to reach its destination. I went for two long drives with my car this summer, once to Italy and once to Brussels, and I didn’t have any issues whatsoever finding a station. But this is Europe, and not the case in many other places, as I learned (more on this later). Within cities, my experience wasn’t that good, though.

Battery ranges are also constantly increasing. With many batteries having a range above 400km, I suspect that range anxiety won’t be a topic anymore soon, especially if charging station networks are being built out further.

The other argument that often comes up is battery lifetime. If I take the analogy of a smartphone, a friend who works at Samsung told me that they should operate at full capacity for at least 500 complete recharges. I only recharge my car 3-4 times per month, so my battery should be good for 10+ years. This is a timeline I am comfortable with.

Europe is leading the electrification wave

This might sound controversial as Tesla is the leading vendor in the West and is based in the US. A VC friend from New York drove with me recently, and he told me that he doesn’t know many people who have EVs in the Big Apple. So I dug deeper. And Europe is way ahead regarding overall accommodation for EV drivers.

The EV market share in 2023 in Europe is 22.3%, while the US is at only 7.2%. And those numbers rapidly on both sides of the pond. The of EVs certainly help. Now, if you look at market shares on both continents, you will see that Volkswagen and Stellantis are the leaders in Europe, not Tesla (even if the Model Y is the top-selling EV).

If you look at the EV charging infrastructure, the difference is even more staggering. In 2023, Europe has around 1.3m public EV chargers, while the US has only 43k. In addition to having more EV chargers, Europe also has a higher proportion of fast charging stations and better distribution. EV users can charge almost anywhere and at a relatively consistent cost. And this gap will remain, with the Biden administration having set a goal of having 500k EV chargers in the US by 2030. Finally, Europe has standardised charging plugs on the Type 2 Mennekes connector, while the US has two competing standards: CCS and Tesla Supercharger. All of this makes it more difficult for EV drivers in the US to find compatible chargers, especially when traveling long distances and in rural areas.

Charging infrastructure in Europe. Source: yannickoswald.com

When it comes to solar panels, Europe is also leading. In 2023, Europe is expected to generate 33% more solar power than the US. Europe has, on average, 1.5 solar panels installed per household, while the US has 1.25. The 33% difference is also partly due to Europe's higher average solar irradiance.

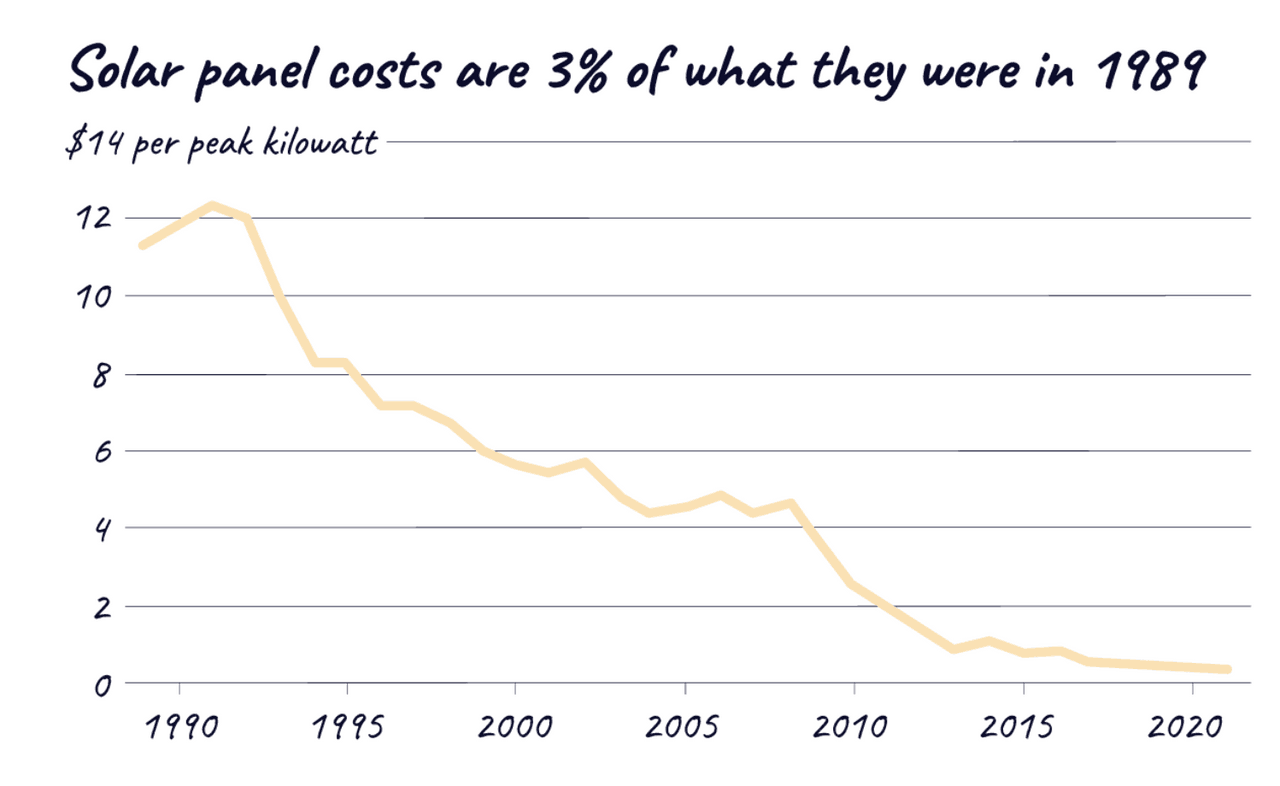

The future looks bright for solar. Solar energy production costs dropped by a factor of 10 since 2010. And this trend will continue, driving further adoption.

Changes in the cost of solar panels; values adjusted for 2021 dollars. Source: Energy Information Administration, BLS CPI Inflation calculator.

I tried both EVs, American (Tesla) and European (BMW). European EVs are underhyped. While the Tesla EV experience is excellent, I can’t claim it is better than BMW’s. Especially in self-driving features (at least in Europe), BMW delivers an equal, if not better, experience.

The big advantage of Tesla is its vast charging network. You can find some Tesla superchargers nearly everywhere you go, removing any potential charging anxiety.

The EV is here to stay, and the trend is bigger than many anticipate. Most automobile manufacturers are making EVs now. They all understand EVs are the future. But there remain real impediments to consumer adoption of EVs. And Europe has put itself in a great spot to lead this trend.

The age of energy decentralisation

When we put all of this in a mixer, what comes out is a huge decentralisation wave. Not only can households now produce their own energy to satisfy their needs, but they will also be able to store it and transport it around in a not-so-far future. A bit like the internet, this creates another wave of decentralisation.

We are transitioning from a centralised electrical grid to a decentralised one. It is a substantial shift in how things are designed. And it is playing out right in front of us. And many smart founders are trying to jump on this train.

Many startups are out there building charging stations and other innovative concepts like Airbnb-like models for chargers. But challenges remain:

1. Making them easily accessible, independent of the network and associated mobile app. If you don’t use a Tesla and their broad charging network, you are in trouble. When you drive from one region to another, the charger operators change. You often need to subscribe to some app you have never heard of, submit your credit card, and hope it works. It happened to me more than once that it did not work. It would make sense for the countries to come together and standardise charging outlets (public and private) at a European level.

2. In my experience, most cities need more charging stations. I also witnessed people blocking them for longer hours than required to charge their car. It is often a pain to find nearby charging stations in many cities.

As electric vehicles become more commonplace, they will likely become platforms akin to the Apple app store that will support a marketplace for new services and apps. For this ‘interface’ to take off, we will have to wait. Fully self-driving cars will most probably be the turning point here, but we are still some years out.

More and more power will be generated by individuals using solar energy. Storage on the edge in homes, cars, etc. will become critical to making the energy transition work. And EVs are a huge storage source that are (mostly) not connected to the grid today. Today, EV charging is one-way only. Those chargers take power from our home (either from our solar panels or the grid) and send it to our EVs. But EVs are huge electricity stores not connected to the grid. As decentralisation moves forward and batteries get better, this will change. There will be many opportunities to build cool services around bi-directional charging and storage.

Electricity is this new commodity everyone can produce and play with. I never thought I could trade my own energy production one day... Homes are becoming these ‘mini utilities’ that make power from the sun and use it to power themselves and trade it. This is also bad news for the legacy utility players who have to run an expensive grid infrastructure and sometimes old-school energy production sites to sell this same utility. Exciting times ahead.

*Yannick Oswald is a partner at leading European venture capital firm Mangrove Capital Partners, best known for its investments in companies such as Wix, Skype, Walkme and K Health. Oswald supports tech startups across Europe and sits on the board of some of Europe's biggest tech start-ups, such as Flo Health, Sifflet and Red Points. In 2020, he launched his blog , with the tagline Opportunities Everywhere, which has become Europe’s most-read VC blog and a key resource for tech entrepreneurs across the continent. He publishes one article a month, usually on a topic related to venture capital and technology entrepreneurship. Yannick grew up in Luxembourg City, has worked in several European countries and the United States, and graduated in commercial engineering in Belgium and Argentina.