An uncertain economic outlook and high interest rates are generally not viewed as a positive backdrop for investment-grade (IG) corporate bonds (rated BBB/Baa and above). Yet, a confluence of supportive factors is underpinning this asset class. These include relatively good credit quality, high average starting yields above 5.5%, an overall duration of about seven years and stabilisation of the banking sector.

As a result, credit spreads above US Treasuries have tightened to slightly less than 120 basis points (bps), which is near their 10-year average of 124 basis points.

In our view, while investment-grade credit could come under selling pressure in an extreme risk-off environment--the duration profile of the sector, credit fundamentals that are better than in prior periods of economic stress, as well as sustained demand from investors--should provide a degree of support, limiting downside risk in most scenarios.

Overall, we believe investment grade provides a solid middle ground for portfolios. If the US Federal Reserve (Fed) executes a “soft landing” and avoids a recession, investment-grade credit should fare well. And if there’s a “hard landing”, the drawdown in investment grade should be muted compared to what we would expect to see in equities. We discuss below each of the factors that are critical to investment-grade credit.

Graphic provided by: Capital Group

1. Duration profile is attractive as Fed hiking cycle ends

Recessionary periods and the end of the Fed hiking cycle have historically been associated with declining rates and spread widening. The Bloomberg US Corporate Investment Grade Index has a duration of 7.1 years, compared to 5.5 years for the Bloomberg US Aggregate Index. This could prove beneficial in a scenario where growth is slowing, leading long rates to rally as the Federal Reserve begins to ease policy.

In the past three economic cycles, yields for both short and long-term bonds have declined before spreads widened. Thus, duration of corporate bonds has helped to offset the impact of wider spreads.

In advance of a potential recession, 10-year US Treasury yields could decline 100 basis points to around 3.5% and credit spreads could widen by a similar amount which would leave investors with relatively low capital losses. The income that investors can currently earn from investment grade, with yields above 5%, would continue to support total returns but may potentially move lower as spreads eventually compressed. These periods of market volatility, however, generally present an excellent opportunity for active security selection to contribute to excess returns.

Graphic provided by: Capital Group

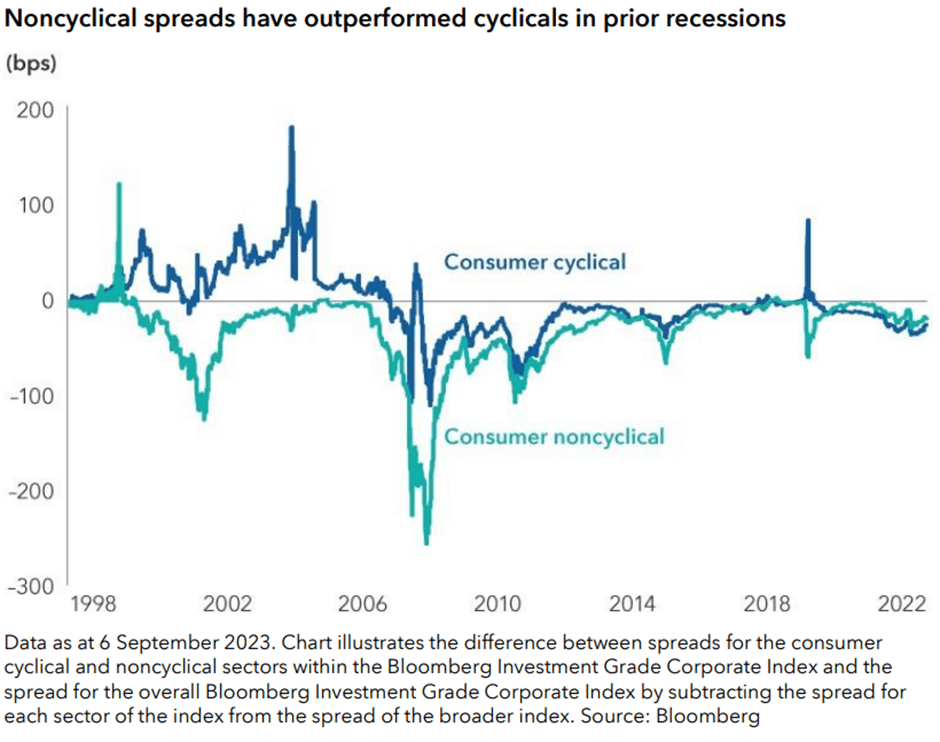

2. Liquidity and a more defensive posture are key amid uncertain economic backdrop

Given an uncertain economic outlook, we continue to emphasise liquidity, partly by allocating to defensive industries that have tended to outperform in challenging economic conditions and focusing on holding on-the-run issues for the credits in our clients’ portfolios.

For instance, recent mergers and acquisitions (M&A) activity in the pharmaceutical sector has created some attractive investment opportunities where large debt deals have come to market at relatively cheap prices. The sector has also held up solidly in prior downturns.

Valuations also currently look compelling for utilities, as spreads have underperformed the broader Bloomberg US Corporate Investment Grade Index due to robust new debt issuance in the first half of 2023. Utility companies’ stable profitability and defensive, regulated business profile should insulate the sector if the economy weakens. Extreme weather is an increasing risk for the sector--with wildfires and hurricanes occurring more frequently--but this risk can be mitigated by credit investors through issuer and security selection.

On the other side, avoiding losers can be just as important as identifying winners. Cyclicals, like chemicals, could be challenged because of the economic backdrop in both the US and China, which have dominated cyclical demand in recent years. We are also limiting exposure to traditional automakers, which have been among the worst performers in the last two recessions.

Graphic provided by: Capital Group

3. High level of absolute yields attracts flows

When yields reach five percent or more on investment-grade corporate bonds, rising inflows into the asset class have tended to create a favourable supply demand dynamic that puts downward pressure on spreads.

Over the year, there has been consistent demand for US dollar-denominated investment-grade credit from US pension funds and international investors, particularly in Asia. Deals coming to market have been many times oversubscribed, despite overall market weakness. Additionally, lower merger and acquisitions activity has resulted in lighter issuance and constrained supply, which has been supportive of valuations.

Many investors who had been underweight to credit are now rebalancing their portfolios, contributing to the demand. We have also seen some investors moving out of equities and buying bonds, particularly among pension funds executing liability-driven investing (LDI) strategies. We expect this favourable technical backdrop to persist, as long as yields remain elevated.

Graphic provided by: Capital Group

4. Financials present opportunities despite challenging Fed policy

At around a third of the Bloomberg Investment Grade Corporate Index, financials are an important part of the investment-grade debt universe, essentially serving as a proxy for the asset class. Given the ongoing funding needs of financials, they are more sensitive to interest rates. Tighter Fed policy typically creates higher funding costs and puts pressure on deposits, which can be a drag on bank profitability. Banks may also see higher losses in their securities books due to higher Treasury yields.

Bank bond valuations are starting to look attractive, but over the near-term, spreads could widen more if the economy weakens, as banks have traditionally not tended to fare well in recessions. Yet, even with a broad downgrade of regional banks occurring in August and some potential headwinds, our analysts remain constructive on the credit fundamentals of select issuers with diversified deposit bases, robust business models and strong risk controls.

Read also

The largest global financial institutions are well-capitalised partly as a result of regulations passed in the wake of the Global Financial Crisis (GFC), which provides an underpinning of support. Meanwhile, the failure of Silicon Valley Bank and Signature Bank earlier this year has continued to cast a shadow on the larger US regional banks. These two areas of banking could provide compelling investment opportunities over the longer term.

If the Fed keeps rates high, smaller banks may come under continued earnings pressure and may experience a few more ratings downgrades. However, over the longer term, these risks will likely be offset by more stringent capital and liquidity rules which would strengthen fundamentals.

5. Credit quality looks solid

Overall, credit quality in the asset class remains solid. Interest coverage is deep and overall leverage is low by historical standards. Refinancing risk is also low, as a large number of companies have locked in debt at lower rates for several years.

The percentage of BBB-rated companies (one step above high yield) in the index has risen from around 25% to nearly 50% over the past three decades, which could be cause for concern. Some cyclical businesses may be at risk of falling into high yield in a recession. Yet, counter-intuitively, companies rated BBB could be at lower risk of a downgrade than in the past.

Incentivised by lower borrowing costs, many single-A companies have been willing to take a downgrade in recent years to fund M&A activity and expand their businesses. But now, sitting at BBB, the management of these companies are incentivised to do everything they can to maintain their investment-grade status as the penalties for falling to high yield are severe. For example, many companies across sectors like pharma, food and beverage, and energy have been focused on reducing debt balances accrued to support acquisitions. In many cases, they would like to maintain the flexibility to do acquisitions in the future which will encourage them to have healthier balance sheets to be able to borrow again in the future at attractive interest rates.

Flavio Carpenzano is a London-based investment director working with the fixed-income team at Capital Group, which has $2.3trn in assets under management globally, including $473.5bn in fixed income funds.